Outlining the journey of M&HCVs for the last 12 years and how they have reflected IIP growth in India, Jayesh Shelar, Head – Product Management Group, Mahindra Truck & Bus Division, Mahindra & Mahindra Ltd, mentioned, “The last decade was one of discovery and presented key challenges like the 3 emission cycles. The BS IV to BS VI emission norm transition was the fastest in the world.” In his presentation as part of the webinar organized by S&P Global Mobility- formerly IHS Markit Automotive- (as part of their 2022 Automotive Solutions Webinar Series) under the theme ‘Indian MHCV Outlook – Is the Future Truly Electrifying’, Shelar expressed that the industry recovered quickly at a GACR of almost 14.8 percent – from the slowdown of FY2014 to the high of FY2019 – by displaying resilience and strong fundamentals. He spoke about the challenge posed by railways starting from 2010. “The rising fuel prices, a shift towards eco-friendly logistics, and an increase in technology have pushed the vehicle cost up,” he added.

Describing the journey of M&HCV segments as a decade of discovery to a decade of disruption, Shelar said, “There were limited brands in India in 2010. By 2030 there will be multiple brand options available.” Drawing attention to a change in the customer profile, he mentioned, “The entry and exit barriers have come down and will ease further. From being acquisition and resale value sensitive in 2010, customers are now looking at Total Cost of Ownership (TCO). They are ready to experiment with new technologies and brands.” Pointing at a shift to higher capacity engines, Shelar said, “A movement towards battery-operated vehicles is also taking place. Fuel cell technologies are catching up and power requirements are ignificantly going up.” Of the opinion that average speeds have gone up and regulations and infrastructure have improved, he informed, “Trucks are traveling up to 450 km a day as compared to 275 km in 2010. By 2030, they will travel up to 700 km per day.”

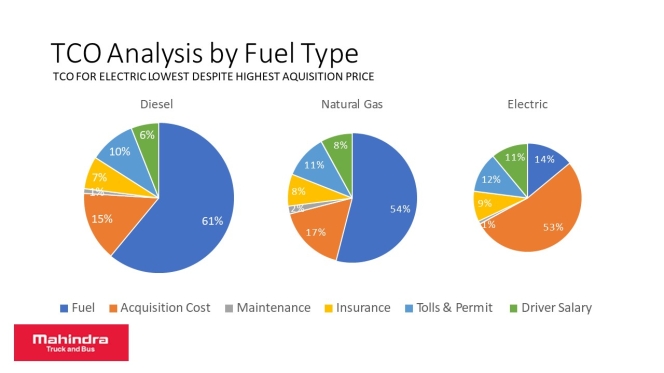

Highlighting rising affinity for technologies like telematics, Shelar mentioned, “A shift from transport to logistics model is taking place.” He drew attention to the TCO of an electric vehicle (despite high acquisition cost) being lower in comparison to the running cost of a diesel and natural gas vehicle over five years. “Fuel cost in diesel and natural gas vehicles is about 55 to 60 percent whereas, in case of the electrical vehicle, it is 14 percent,” quipped Shelar. Underlining the government’s pledge to be net zero by 2030 through measures like 500 gigawatts of non-fossil fuel electricity generation and an increase in natural gas production among others, he said, “Electric vehicle technology is relevant event though issues like high initial acquisition price and charging time will take some time to resolve.”

Drawing attention to key drivers like the FAME policy, stringent emission norms, higher compliance cost, and new business models against challenges like the high initial acquisition cost of EVs, range anxiety, developing charging infrastructure, and battery performance, Shelar said that fuel cell is the long-term technology for M&HCVs. In his presentation, Paritosh Gupta, Analyst – M&HCV Forecasting, S&P Global Mobility, averred that the global M&HCV industry headwinds include the Russia-Ukraine conflict and supply chain constraints. “The forecast for 2022 alone is a drop of about 150,000 units, which is 4.4 percent of the entire market size,” he added. Informing that major degradation has come from Europe and North America, Gupta mentioned, “In 2022, the European and North American markets have dropped by 86,000 units and 38,000 units respectively. A lot of volume from central and eastern Europe has been lost and the possibility of sales moving up smartly in the next three years is less.”

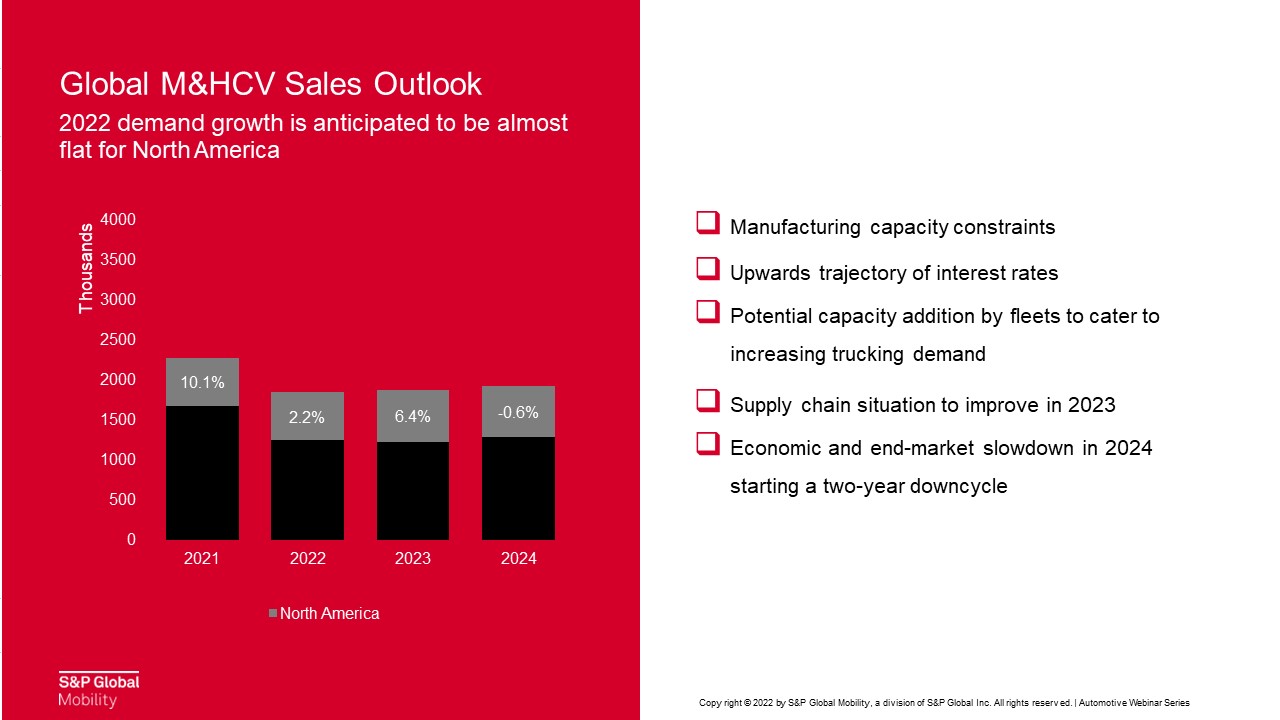

Stating that South Asia, Middle East, and African regions are showing optimism, he explained, “The South Asian market is primarily driven by the performance of the Indian market over the last two quarters. The Chinese market was the only one in 2020 among the key regional M&HCV markets to report positive growth numbers.” Underlining China’s slowing economic growth due to factors like a highly stringent pandemic policy, ithdrawal of pandemic state support, and a shift from road to rail for bulk materials, Gupta expressed, “A 26 percent drop in 2022 and another 1.6 percent drop in 2023 is expected before recovery starts in 2024,” Announcing that the North American forecast is largely positive even though the potential for growth remains limited, he stressed on rising inflation, increasing interest rates, and manufacturing constraints. “We expect fleets to add capacity with the supply chain situation improving in 2023,” quipped Gupta.

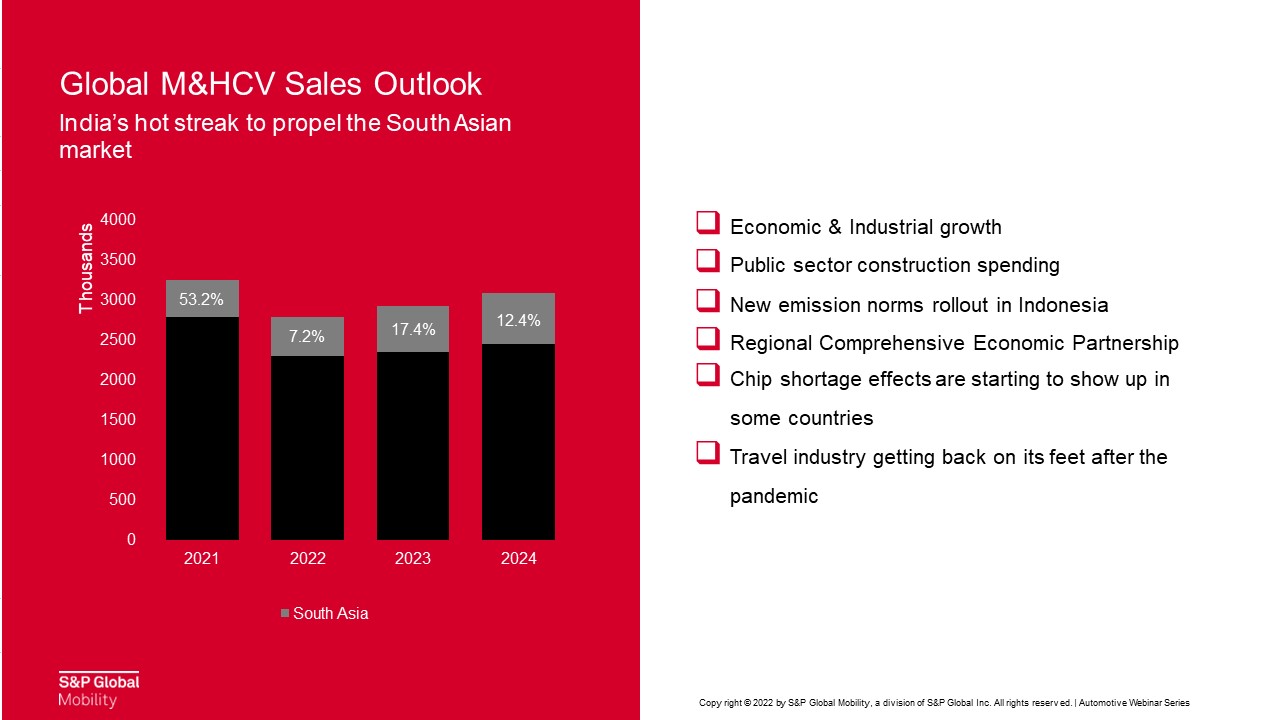

Describing that the Western European market is estimated to remain flattish while the Central and Eastern European market is estimated to drop by 28 percent, Gupta pointed at the Russia-Ukraine conflict and supply constraints as the reasons. Western European markets are facing challenges like raw material and truck price increase whereas the Eastern-Central European markets are facing sanctions, stoppage of production by foreign OEMs, and the possibility of Chinese OEMs setting up shops in Russia, he said. Stressing that South Asia was the fastest growing market in 2021, led by India outgrew expectations, Gupta revealed that India accounts for around 60 percent of the M&HCV sales in the region. “In 2022, the South Asian M&HCV market should grow by 7.2 percent and the figures for 2023 and 2024 will be healthy double-digit ones,” he explained. Of the opinion that the factors driving the South Asian M&HCV market include economic and industrial growth, public sector construction spending, the roll-out of new emission norms in Indonesia, comprehensive economic partnership across the region, and an increase in travel, Gupta quipped, “Struggling with chip and other raw material shortage, the Japanese and South Korean markets are expected to be largely flat.”

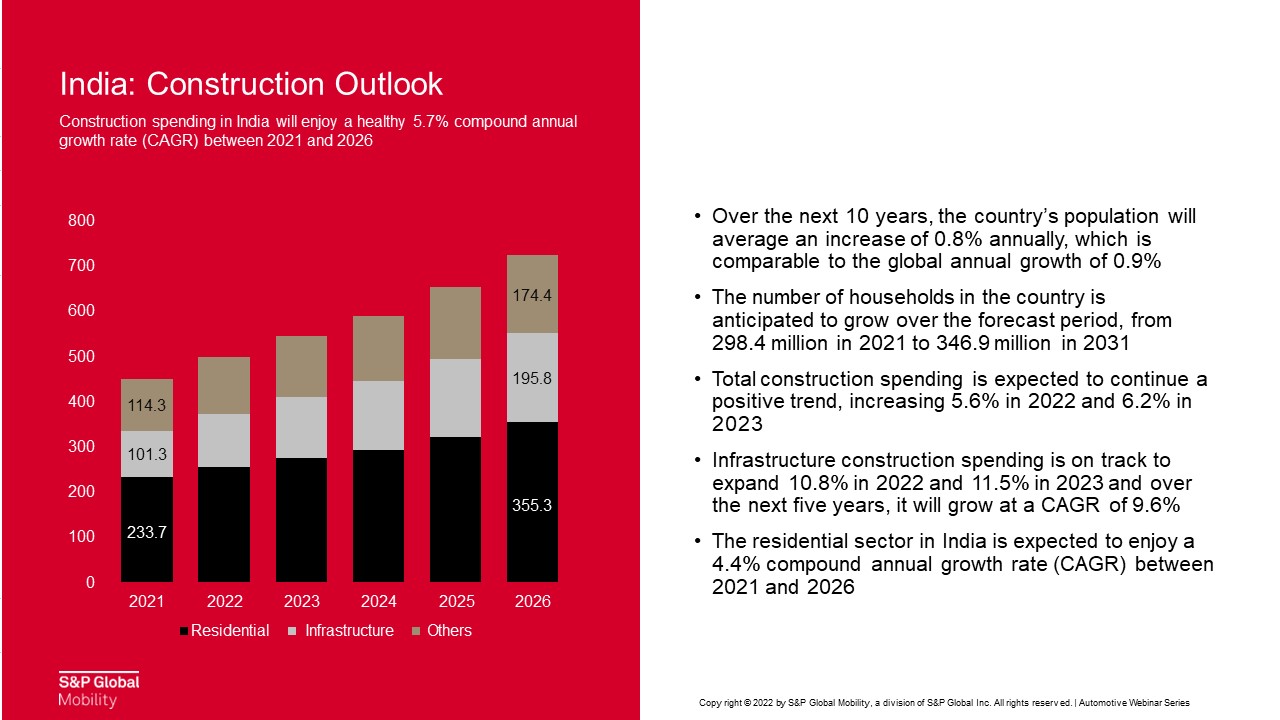

Highlighting rising inflation, high import bills, and weaker global demand as Indian M&HCV headwinds, Gupta mentioned, “The outlook is largely positive though not to the extent it was two years back.” “The construction industry spending will command a CAGR of 10.1 percent between 2021 and 2026 and provide a solid impetus for M&HCV growth,” he added. Stating that while the infrastructure segment’s growth will fuel the growth of heavy-duty trucks, Gupta quipped, “The upward growth trajectory of the e-commerce industry towards becoming the second largest by 2034 is indicative of the growth in demand for medium-duty trucks.” Explaining that the rise of e-commerce and medium-duty trucks over the last five years is a parallel journey, he averred, “Expected to grow at a CAGR of 21 percent over the next 8 years as per IBEF, the e-commerce industry will give a huge boost to medium-duty trucks in India in the future.” “The government has also introduced several policies which are aimed at providing growth to the automotive industry,” he added.

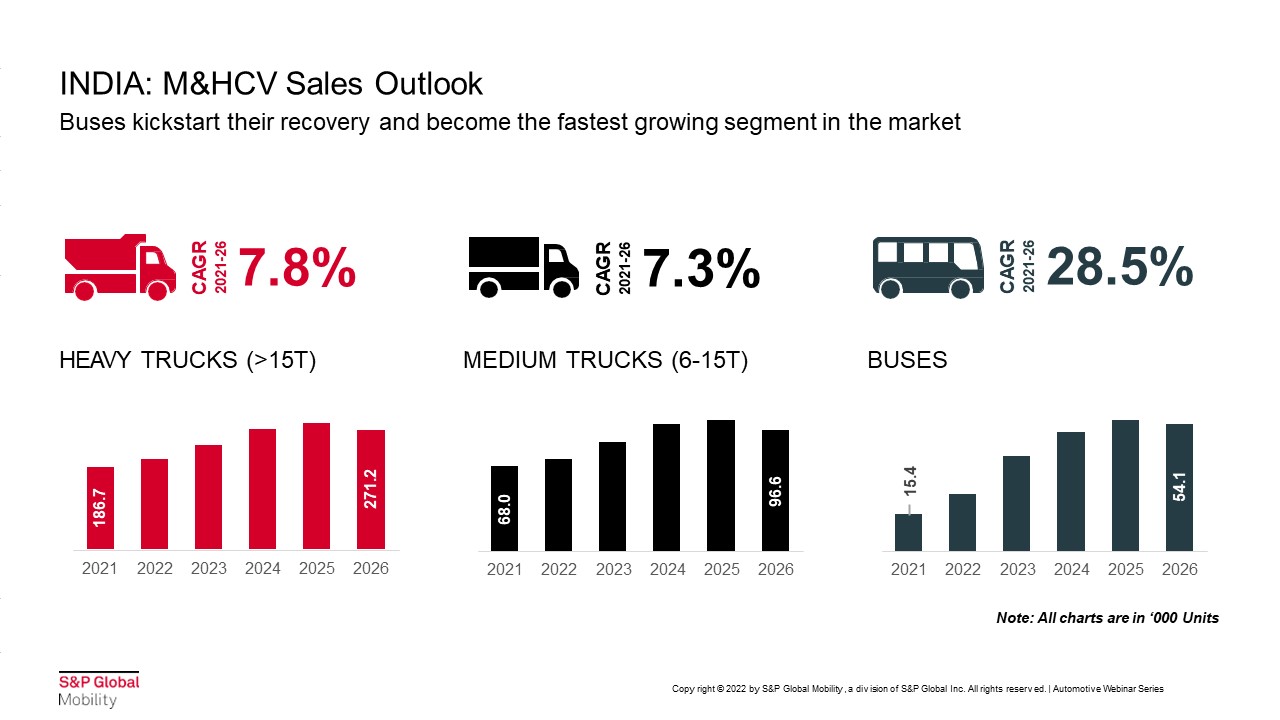

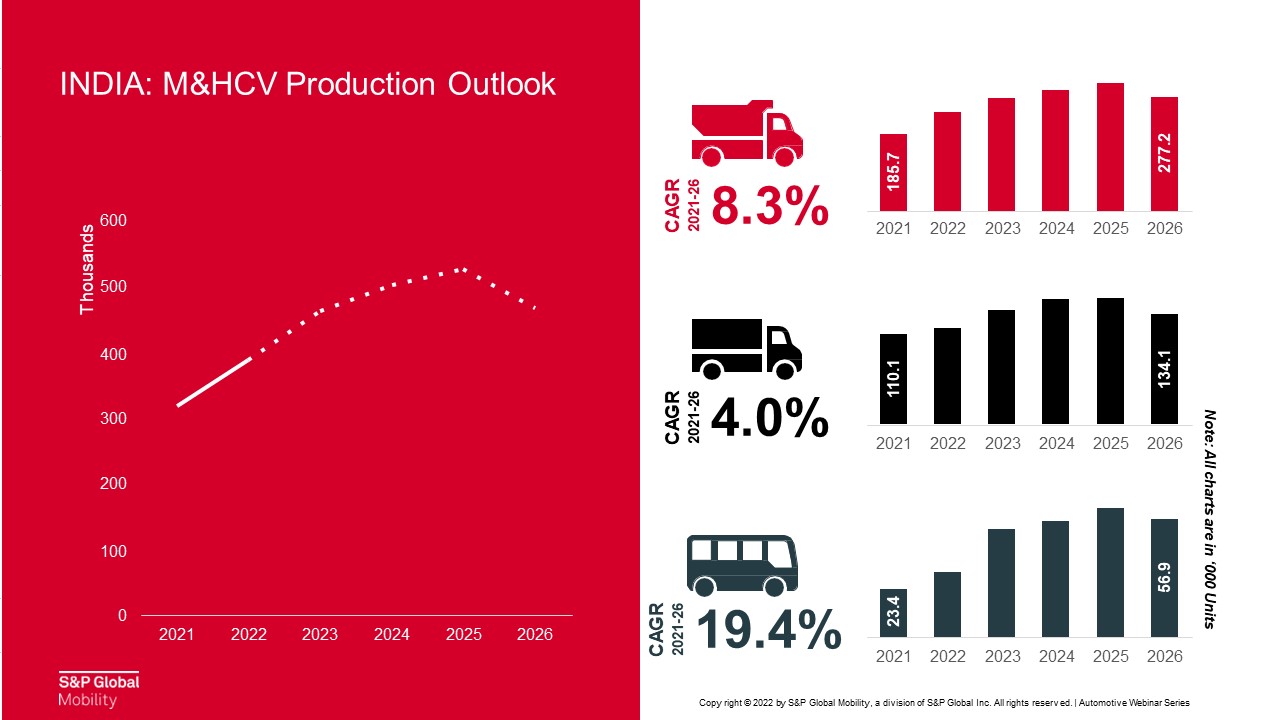

Pointing at the scrappage policy, production-linked incentive scheme, and electrification initiatives, Gupta said, “We see a big tranche of about 50,000 e-buses to come over the next five years” Of the opinion that the monopoly of Tata Motors and Ashok Leyland will continue over the next decade, he averred, “Expect the industry volumes to peak in 2025. Tata Motors will almost touch 200,000 units in 2026.” “In terms of segmental sales, heavy trucks are the largest shareholder in the (M&HCV) market and are expected to clock 275,000 units in 2026 growing at a rate of 7.8 percent,” quipped Gupta. Explaining that MCVs rise will be linked to the rise of e-commerce industry growth and will clock almost 97,000 units by 2026 at a rate of 7.3 percent, Gupta said, “Worst hit by the pandemic, the M&HCV bus segment is expected to pick up in 2022 and reach 54,000 units by 2026.” “The production trend of M&HCVs will be similar to the demand trend in the market. Some buffer will be provided by exports as part of the PLI scheme,” he added.

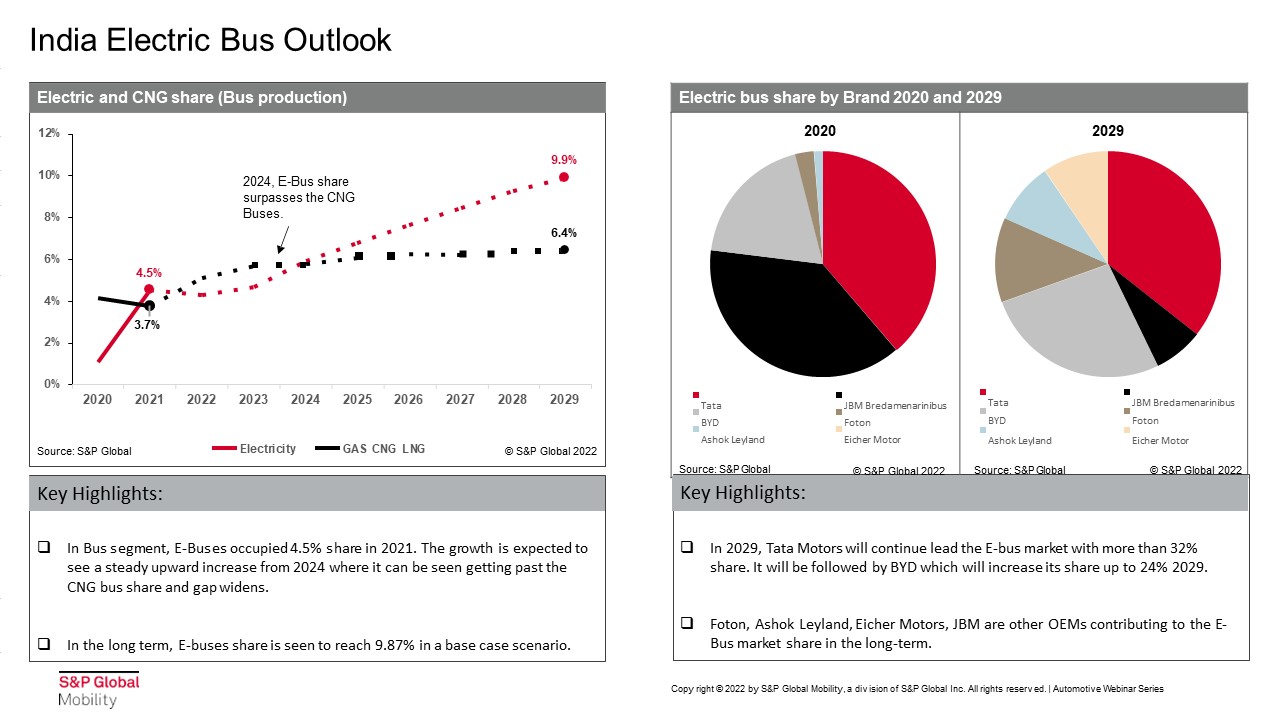

On the topic of M&HCV propulsion trends, Manat Bali, Research Analyst, S&P Global Mobility, mentioned, “Electrification is happening at a much higher pace in buses than trucks. About 99 percent of the M&HCV truck market is currently belonging to IC engines comprising gas and diesel fuels. About 75 percent of the bus market is driven by IC engines running on gas and diesel. With electrification initiatives, the market share of e-buses is expected to reach 30 percent in the long run. It will reach about 9.8 percent by 2029. Natural gas market share will increase up to 12 percent by 2029, triggered mainly by increased availability. It will achieve better traction in medium-duty trucks rather than in heavy-duty ones.”

Of the opinion that diesel fuel will see a de-growth of about 9 percent by 2029 in the Indian CV market at the cost of gas and electrification, Bali averred, “The only electrification taking place in the M&HCV segments is in the bus space as of now. In the long-run, the CNG market share will continue to trail that of the e-bus market share.” “Tata Motors will continue to lead the e-bus market followed by BYD and others in the long run,” he added. About the global e-bus market in the M&HCV category, Bali mentioned, “China is a highly ature and dominant player in e-buses. Other regions are moving up with South Asia having a CAGR growth of 46 percent from 2020 to 2029. India will dominate the e-bus market in South Asia by contributing to over 90 percent of the share.” “The factors driving electrification in India include FAME, state schemes, COP26 target, PLI schemes, and taxation,” he added. “The hindrances in electrification include regulatory drawbacks, infrastructure issues, cost concerns, and end-user dilemmas,” Bali concluded.

Recorded webinar session Available on Demand, please click the link below to watch the session:

https://event.on24.com/wcc/r/3673674/7F886C4E4B36403DD80C623612674EFF?partnerref=motoringtrends

- TVS VMS

- TVS Vehicle Mobility Solutions

- Montra Electric

- Montra Electric Rhino

- Jalaj Gupta

- Navneet Sethi

- Madhu Raghunath

TVS VMS Partners Montra Electric To Deploy E-Trucks For Freight Operations

- By MT Bureau

- August 07, 2026

TVS Vehicle Mobility Solutions (TVS VMS) has entered into electric commercial trucking through a partnership with Montra Electric, deploying a fleet of Montra Electric Rhino heavy commercial vehicles into freight operations.

As part of the initial phase, TVS VMS flagged off 57 Montra Electric Rhino 5538 EV 4x2 TT trucks in Manesar. The electric heavy commercial vehicles will operate on a primary freight route covering a 190-kilometre distance in Chhattisgarh, supported by three charging stations along the corridor. The partners are targeting to expand the deployment to more than 300 electric trucks in FY2026–27.

Jalaj Gupta, Managing Director, Montra Electric, said, "For a partner like TVS VMS, with seven decades of experience to put our electric trucks into live freight operations is exactly the validation India's logistics industry needed. This is proof that our technology is ready for commercial scale. It also reflects the depth of what we've built at Montra Electric with products engineered to address the specific operational needs of this market. Our team worked with TVS VMS to plan the operations, set up charging around their exact routes, and our telematics platform keeps optimising performance as the fleet runs. That's the difference between a truck that works on paper and a fleet that works on the road."

Navneet Sethi, CEO, Montra Electric (eM&HCV Division), said, "For years, industries built around heavy, continuous haulage, steel being a prime example, have questioned whether electric HCVs can genuinely stand up to sustained heavy-load freight, and that scepticism has shaped how slowly this sector has moved toward electrification. TVS VMS putting our Rhino trucks into live operations answers that question decisively, for us and for every heavy-load industry watching closely. This is a company with over seven decades of running conventional trucking now choosing to enter electric trucking for the first time, and choosing us to do it is validation that our platform can handle the demands of commercial-scale freight. For Montra Electric, this is a marker of how electric heavy trucking moves from possibility to standard practice in India, and we intend to lead that shift at national scale."

Madhu Raghunath, CEO, TVS VMS, said, "This strategic partnership marks a decisive step in advancing India's green logistics infrastructure. TVS Vehicle Mobility Solutions is proud to power this transition through our full-suite, end-to-end lifecycle management platform—integrating vehicle leasing, driver operations, maintenance, insurance, charging ecosystem, and connected telematics to make zero-emission fleet operations effortless and commercially viable."

Manufactured at the Montra Electric facility in Manesar, the Rhino 5538 EV tractor-trailer features a 55-tonne gross combination weight capacity. It incorporates a 282 kWh lithium iron phosphate battery paired with a permanent magnet synchronous motor delivering 280 kW peak power and 2,000 Nm torque. The vehicle offers a range of up to 198 km per charge under loaded and empty cycle conditions, and is available in fixed-battery fast-charging and battery-swapping configurations.

Belrise Industries Acquires Hyva India’s Tipper Body Business For $5.65 Million

- By MT Bureau

- August 04, 2026

Automotive and aerospace component manufacturer Belrise Industries has announced the acquisition of the Tipper Body Business of Hyva India, a subsidiary of JOST Werke.

The transaction carries a total purchase consideration of approximately USD 5.65 million, representing an Enterprise Value to EBITDA multiple of approximately 3.60x.

Hyva India manufactures tipping solutions used across construction, mining, defence and infrastructure sectors, supplying the top five commercial vehicle original equipment manufacturers in India. The business reported EBITDA of approximately USD 1.57 million for calendar year 2025, alongside a return on average capital employed of around 20 percent.

Through the acquisition, Belrise expands its manufacturing footprint by adding three production plants located in Pune, Jamshedpur and Bengaluru. The deal also incorporates a European commercial vehicle original equipment manufacturer into Belrise's client portfolio as part of its positioning as a Tier-0.5 supplier.

Swastid Badve, General Manager, Belrise Industries, said, “We are pleased to welcome Hyva India’s Tipper Body Business into the Belrise family. This acquisition is a strong strategic fit and complements our manufacturing and engineering strengths. It enhances our position in the commercial vehicle value chain and supports our vision of becoming a diversified, global mobility solutions provider. Belrise remains committed to ensuring a seamless transition for customers, employees, suppliers, and business partners, while investing in the future growth and development of the business.”

Flytta Green Deploys Electric Trucks For Dalmia Cement In Assam

- By MT Bureau

- August 04, 2026

Logistics company Flytta Green has introduced a fleet of heavy-duty electric trucks for Dalmia Cement's clinker transportation operations in Assam. The deployment is being executed in partnership with Drivn, which is providing financing and leasing options for the vehicles.

The initiative follows Flytta Green's introduction of retrofitted electric trucks for Dalmia Cement in October 2025. The company's strategy focuses on deploying new electric trucks with a gross vehicle weight of 55-tonnes and above, alongside developing charging infrastructure and exploring solar power integration for fleet operations.

The initial delivery of 15 trucks, manufactured by Montra Electric, was completed last week. An additional 45 vehicles are scheduled for delivery during August and September.

Flytta Green has received expressions of interest for approximately 1,000 heavy-duty electric trucks, with planned deployments spanning the next 18 months across the cement, mining and metals sectors. The initiative is being managed by Ashwin Dichpally, Chief Operating Officer of Flytta Green.

In collaboration with Drivn, Flytta Green plans to deploy 200 trucks during the current financial year, with financing for subsequent vehicles to be funded by international investors. Deployment operations will prioritise the North-East, East and South-East regions of India.

- Switch Mobility

- Hinduja Group

- Sai Green Projects

- PM E-Drive

- BEST

- Brihanmumbai Electric Supply and Transport

- Pune Mahanagar Parivahan Mahamandal

- PMPML

- Ganesh Mani

- RG Venkataraman

- Vikas Gupta

Switch Mobility Secures Order For 650 E-Buses From Sai Green Projects

- By MT Bureau

- July 30, 2026

Switch Mobility, the electric vehicle subsidiary of Hinduja Group, has secured an order to supply 650 electric buses to transport operator Sai Green Projects. The e-buses will be deployed for public transit operations in Mumbai and Pune under Phase II of the Government of India's PM E-Drive scheme.

Under the supply agreement, Switch Mobility will deliver 9-metre electric buses procured through the CESL PM E-Drive Phase II tender framework. Sai Green Projects won the operational rights to run the fleet, which comprises air-conditioned and non-air-conditioned variants. The buses will serve routes managed by the Brihanmumbai Electric Supply and Transport (BEST) undertaking in Mumbai and Pune Mahanagar Parivahan Mahamandal (PMPML) in Pune.

Ganesh Mani, Chief Executive Officer, Switch Mobility, said, "The deployment of 650 electric buses is a significant step towards India’s ambition to reduce emissions, improve operating economics, and modernise public transport systems. At Switch Mobility, we remain focused on delivering reliable and efficient electric mobility solutions that enable operators to transition towards cleaner public transport while ensuring a superior passenger experience. With a growing product portfolio, we are well positioned to support the evolving mobility requirements of cities across India."

"We are pleased to partner with Sai Green Projects in supporting large-scale deployments in Mumbai and Pune under the PM E-Drive initiative. This is the beginning of a long-term partnership where we look forward to covering many green miles together," added Mani.

RG Venkataraman, Chief Commercial Officer, Switch Mobility, said, "This development is a strong testament to our commercial proposition and our ability to deliver at scale for operators across the country. At Switch Mobility, we go way beyond manufacturing great products. Our focus is to make sustainability commercially viable to the operators so they can run efficient, profitable fleets."

Vikas Gupta, CEO, Sai Green Projects, said, "Sustainable living is at the core of what we do at Sai Green Projects. We are proud to partner with a leading OEM like Switch Mobility to take India's vision for clean, efficient, and future-ready public mobility forward. We are confident that these electric buses will enhance the everyday experience of commuters in Mumbai and Pune."

The contract expands Switch Mobility's operational footprint in India, where the manufacturer has supplied over 2,500 electric buses to date across city, intercity and specialised transport segments.

Comments (0)

ADD COMMENT